This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful. Cipher is now part of the Lexis Nexis Intellectual Property and will be adhering to their privacy policy

27th February 2019

Having problems scouting start-ups? New Lidar report

The automotive industry is being disrupted at an unprecedented rate, and no single OEM or Tier1 supplier can innovate, even less lead, in all areas. Disruption in electric and connected cars is happening now: partnerships, collaborations and acquisitions are all necessary are required to join the quest to the autonomous vehicle. New players are driving the innovation agenda, shifting from Detroit and Germany to Silicon Valley bursting with software and hardware start-ups.

Incumbents are increasingly feeling the pressure. Since 2016, there has been a surge in acquisitions and investments. Continental acquired ASC’s 3D Flash Lidar division in 2016; Ford invested $1B in Argo, GM acquired Strobe in 2017 following on the 2016 acquisition of Cruise not forgetting course, the Intel’s acquisition of Mobileye.

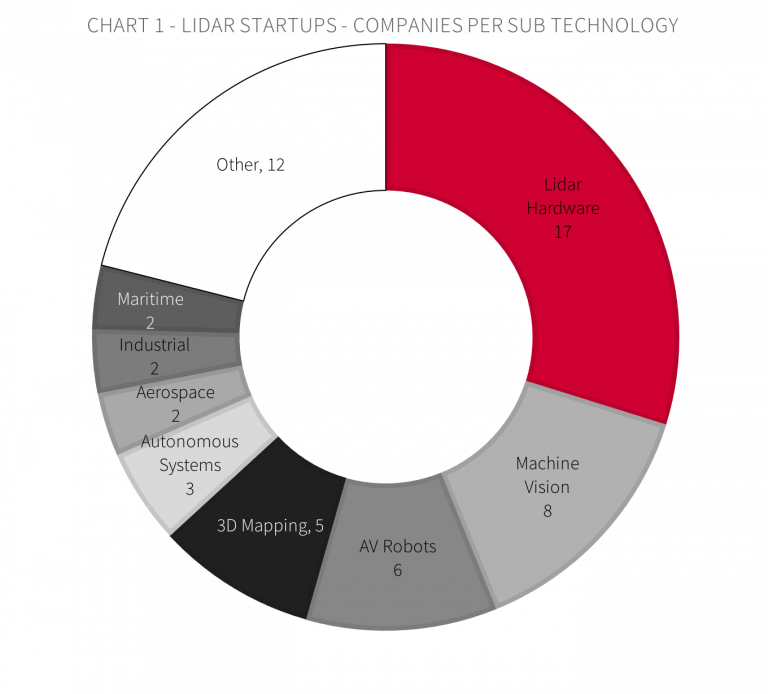

Our recent analysis has identified 56 start-ups in the Lidar space working in a number of different sub-areas, seen in Chart 1 below, with 17 of them working with Lidar hardware. So the question is can OEMs and suppliers afford not to know what these companies are doing?

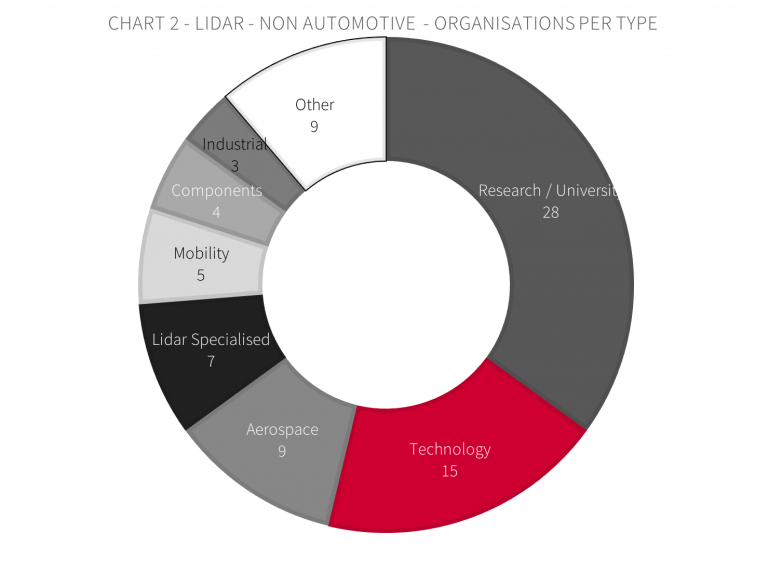

Acquisition and investment is only one of the tried and tested business models. Our Lidar Report identifies plenty of collaborations – 63 in total. Many of the organisations investing in Lidar are outside the automotive ecosystem, including Apple, Baidu, Google and Qualcomm. In addition, there are specialised larger Lidar and Sensor companies like Hexagon, IHI and Sick that have very significant patent portfolios in this area as seen in Chart 2.

Cipher Automotive has launched a Start-up Finder service to help companies identify the companies active in specific automotive technologies. Patent information is uniquely placed to answer this question as it has the following unique properties:

- Global – you are not limited to Silicon Valley unicorns, and all data had been normalised to English

- Identify collaborations – who’s working with who?

- Corporate and University research – find pockets of innovation in large companies

- Full technical details – not just trend data, but also detailed technical descriptions

- Quantifiable – who are early inventors, who’re surging now, how specialised in Lidar are they?

- Key inventors – not only looking at organisations but also the most prolific inventors in each organisation.

To download a copy of our 30 page Start-Up Finder Report click here